How to Pay 0% on Capital Gains with Puerto Rico’s Act 60

Author

Joel Ortega is a tax advisor and compliance strategist specializing in Puerto Rico’s tax incentive programs and corporate structuring. A graduate of the University of Puerto Rico with a Bachelor’s in Accounting, he previously held roles at top accounting firms before co-founding Imperium Management Group. At Imperium, he leads the firm’s tax strategy and client advisory services, working closely with high-net-worth individuals and businesses navigating Act 60 and other complex financial frameworks.

Imagine selling crypto, stocks, or your business and paying 0% capital gains tax. That’s exactly what Puerto Rico’s Individual Investor Incentive (Act 60) offers to those who relocate to the island and meet specific criteria. For investors, founders, and high-net-worth individuals, this can mean millions in tax savings—but timing and structure are critical.

What Is the Individual Investor Incentive?

Under Act 60 (formerly Act 22), qualifying individuals who establish bona fide residency in Puerto Rico can enjoy:

100% tax exemption on capital gains from assets acquired after becoming a resident

No U.S. federal capital gains tax under IRC Section 933

No Puerto Rico capital gains tax on qualifying income

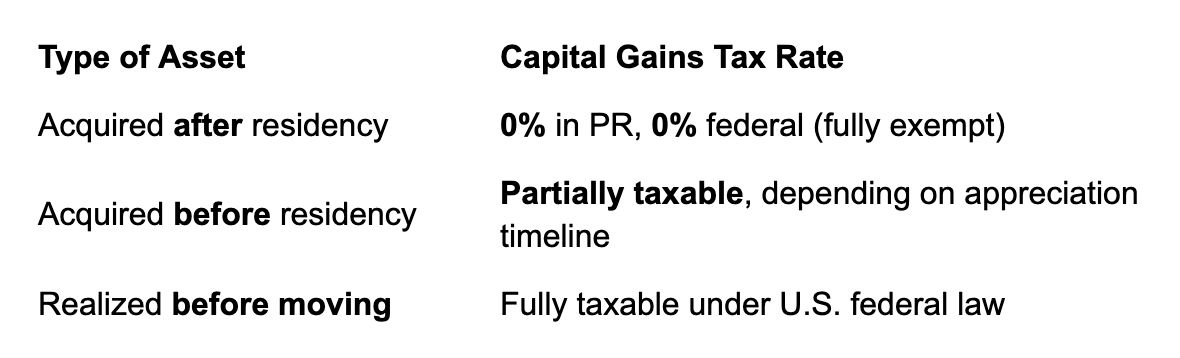

Gains on assets acquired before becoming a resident may still be partially taxable depending on sourcing and holding period.

Who Qualifies for the 0% Rate?

To qualify, you must:

Be a bona fide resident of Puerto Rico

Have acquired the capital assets after becoming a resident

Apply for and receive an Individual Investor Tax Exemption Decree from DDEC

Make annual charitable donations totaling at least $10,000 to approved Puerto Rican nonprofits

Purchase a residential property in Puerto Rico within two years of receiving the decree

Capital Gains Timing: The Crucial Distinction

What About Dividends and Interest?

Act 60 also offers powerful tax treatment for interest and dividends:

Puerto Rico–sourced interest and dividends are 100% tax-exempt in both Puerto Rico and the U.S.

�U.S.–sourced interest and dividends remain taxable in the U.S., even if you are a Puerto Rico resident

Example:

Interest earned from a Puerto Rican bond = 0% tax in both PR & U.S.

Dividends from U.S. stocks (e.g., Apple, Tesla) = Taxable by IRS, not by PR Treasury

Examples of Qualifying Capital Gains

Sale of publicly traded stocks

Crypto assets acquired after relocation

Startup equity or carried interest earned post-move

NFTs, art, and collectibles

Gains on real estate (if Puerto Rico–sourced)

Residency Requirements: What the IRS Looks At

To become a bona fide resident, you must pass these three tests:

Presence Test – Spend 183+ days per year in Puerto Rico

Tax Home Test – Your primary business or professional activity is located in PR

Closer Connection Test – Your social, family, and financial ties are stronger in PR than anywhere else

Warning: Failure to pass these tests risks losing the tax benefits and triggering IRS audits.

Common Pitfalls to Avoid

Selling appreciated assets before becoming a resident

Failing to meet the annual donation or property purchase requirements

Keeping primary ties (home, bank accounts, family) in the mainland U.S.

Assuming Puerto Rico residency without IRS-compliant evidence

.jpg)